.jpg)

Subsidiaries

UBM

UBM

If this is your company, CONTACT US to activate Packbase™ software to build your portal.

New research launched at CPHI Milan – the world’s largest pharma event, which was held at Fiera Milano (October 08-10, 2024) – forecasts promising growth for biotech and pharma markets in the coming year, bringing growth opportunities for outsourcing providers.

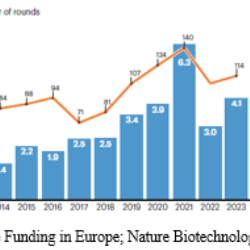

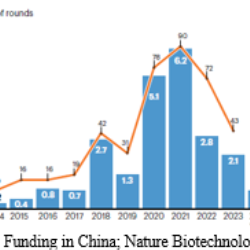

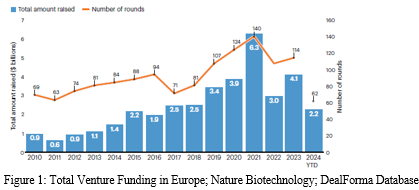

The event arrives at a pivotal moment, with data indicating a strong 2025 outlook, particularly for larger CDMOs and those with U.S.-based assets or specialised technologies such as peptides and radiopharmaceuticals. Notably, European biotech has led the way in 2024, securing strong venture funding compared to the past two years and is set to surpass all prior years, excluding 2021 (Figure 1). In fact, even U.S. investors, traditionally focused on domestic opportunities, are increasingly turning their attention to Europe and the UK for emerging hubs of innovation. In contrast, China’s venture market continues to decline, trending toward 2019 levels and well below the peaks of 2022 and 2023 (Figure 2).

Tara Dougal, Brand and Content Director at CPHI Milan, commented:

“We are witnessing a record-breaking event this week, with unprecedented levels of partnering across the industry. European biotech hubs are expanding rapidly and securing crucial funding, and CPHI Milan will play a key role in helping these groups connect with the right partners to advance their projects.”

CPHI Milan is hosting over 600 CDMOs, attracting a growing number of investors and thousands of biotechs seeking partners. The event is widely viewed as a key indicator of the sector's growth prospects in the year ahead.

As predicted in last year’s report, biotech venture funding has recovered during the first two quarters of 2024, with significant improvements in ‘follow-on’ funding compared to 2022 lows. However, IPO activity remains sluggish, with rates well below pre-pandemic levels.

Analysis was provided by CPHI Annual Report expert Brian Scanlan of Edgewater Capital, who noted that “overall cash runways are improving, alongside favourable economic conditions and interest rate cuts. This, in turn, should prompt biotechs to return to more traditional spending patterns, with CRO/CDMOs benefiting from increased confidence in the financial outlook over the next 12 months.”

Funding is, however, not being distributed evenly. While CDMOs focused on later-stage and commercial projects are experiencing better growth, early-stage biotechs and smaller CDMOs, particularly those in pre-clinical and clinical stages, are facing more challenges. Additionally, with IPOs remaining weak, companies with de-risked assets are finding more favour with both investors and pharma companies.

In a further boost for large CDMOs, big pharma continues to cut R&D resources, favouring outsourcing as a medium-term solution. The growing demand for GLP-1 production and CDMOs specialising in fill-finish and peptide manufacturing are likely to see strong commercial interest in the next 18 months. CRO/CDMOs focused on therapeutic modalities like ADCs, biologics, and small molecules—rather than cell and gene therapies—are also expected to experience increased momentum through 2024 and into 2025 as ‘safer’ bets.

Specialised CRO/CDMOs, particularly those with expertise in radiopharmaceuticals and peptides, are poised for growth. The high barriers to entry in these areas could create a supply-demand imbalance as more complex radiopharmaceuticals and peptides enter clinical pipelines.

This news is a timely boon for CPHI Milan attendees, and Tara Dougal, Brand and Content Director, Pharma at Informa Markets, added: “The partnerships formed over the next three days will be crucial for the sector's growth in 2025. Across the show floor, we’re witnessing rising confidence levels, and the long-term outlook for the industry is incredibly strong.”

Despite positive trends, challenges remain. The biotech sector continues to be saturated with companies competing for the same funding. Although some consolidation has occurred, the number of companies with active R&D pipelines has grown throughout 2024, now surpassing 6,000 globally. Over 50% of these companies have only one or two products in development (Figure 9), making them less attractive in the current market to investment

To download the full CPHI Annual Report, please visit: https://www.cphi-online.com/the-cphi-annual-report-2024-once-again-highlights-file151354.html

See also

.jpg)

.jpg)